Corporate and investment banking (CIB) is entering what may be its most consequential transformation since the post-2008 regulatory reset. But this time, the pressure is not coming from regulators but from clients, competitors and the very architecture of digital finance itself.

According to the Capgemini Research Institute’s inaugural World Corporate and Investment Banking Report 2026, the traditional advantages of banks – scale, balance sheets and regulatory moats are no longer enough. In fact, they may increasingly be liabilities. The industry is not just evolving. It is being rewired.

For decades, corporate banks thrived as intermediaries. Today, that model is under siege.

The numbers tell the story starkly. Only 23 per cent of corporate clients believe banks meet their expectations, while a staggering 85 per cent are already engaging or planning to engage with non-bank financial institutions (NBFIs) within the next year.

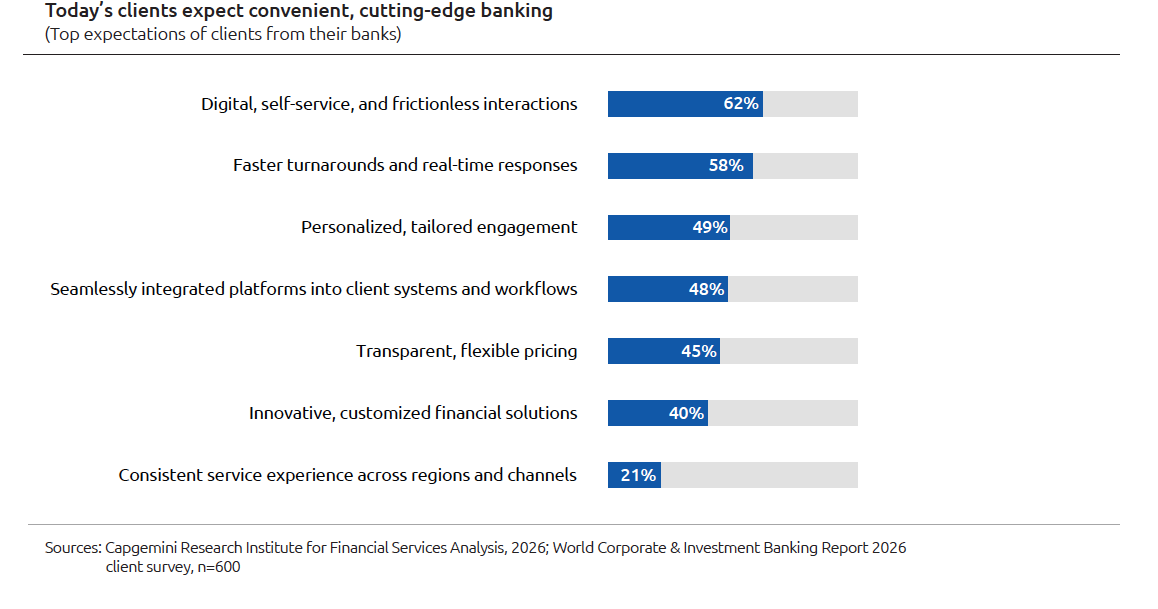

What clients want is no longer controversial: real-time responsiveness, seamless integration into ERP and treasury systems, and personalised, data-driven insights. Yet banks are structurally unable to deliver. Legacy infrastructure consumes 43 per cent of IT budgets, while only 29 per cent is allocated to transformative technologies.

The emerging winners, as the report argues, will not be “better banks” in the traditional sense. They will be client-centric capability orchestrators: platforms that integrate data, workflows and ecosystems into a unified experience. This shift echoes a broader pattern across deep tech: from products to platforms, and from ownership to orchestration.

The real threat is not fintech but disintermediation

For years, fintech disruption has been framed as a battle between startups and banks. That framing now feels outdated.

The real threat is subtler and more dangerous, which is the loss of interface control.

Fintech platforms, API aggregators and treasury systems are increasingly becoming the operational layer through which corporates interact with financial services. Banks, meanwhile, are being pushed into the background as utility providers.

Consider this: platforms like Kyriba processed US$15 trillion in transactions in 2024 alone, embedding payments, liquidity management, and forecasting directly into enterprise workflows.

When financial services become embedded, the institution that owns the interface owns the relationship. Banks are discovering, perhaps too late, that their greatest competitive advantage was never capital. It was proximity to the client. And that proximity is now being intermediated away.

AI is not the differentiator

If there is one area where banks appear to be investing aggressively, it is AI. But here too, the reality is less encouraging. Despite years of investment, 82 per cent of banking executives say innovation initiatives are not delivering new revenue, and over half report no meaningful cost savings.

The problem is not AI itself. It is the inability to industrialise it. Only 26 per cent of banks have centralised AI governance, leading to fragmented experimentation and stalled deployments. In many institutions, AI remains trapped in proof-of-concept purgatory – impressive demos with limited operational impact.

Meanwhile, clients remain sceptical. Nearly 89 per cent question the reliability of AI-generated outputs in banking contexts. This exposes a critical paradox: banks need AI to compete, but without trust and governance, AI adoption itself becomes a risk.

The institutions that break this deadlock will treat AI not as a feature, but as an orchestration layer that embeds AI across workflows, decision making and client interactions. As highlighted in the report, AI-driven workflows, real-time treasury systems and tokenised assets are already emerging as key battlegrounds.

The quiet rise of private capital and tokenised finance

While fintech reshapes the front-end, private capital is quietly reshaping the back-end economics of banking.

Private credit has moved from niche to mainstream, capturing a growing share of leveraged finance deals. At the same time, non-bank trading firms are expanding rapidly, with projections suggesting they could account for 30 per cent of global trading volumes by 2030.

Banks are responding through partnerships, hybrid financing structures and internal investment vehicles. But these are defensive moves. The more fundamental shift is towards new asset classes and infrastructures, particularly tokenisation.

More than half of banking executives are now exploring tokenised products, recognising their potential to unlock new fee streams through digital custody, issuance, and 24/7 settlement capabilities.

Tokenisation, in this context, is not hype. It represents a convergence of capital markets, blockchain and real-time finance: one that could fundamentally alter how value is issued, traded and settled.

Culture may be the biggest bottleneck

Perhaps the most underappreciated finding in the report is not technological but cultural.

Nearly 40 per cent of executives cite conservative organisational culture as a barrier to innovation, while only 23 per cent are investing in internal reskilling. Instead, many banks are opting to hire external AI talent, which is a strategy that may accelerate capability in the short term but does little to transform institutional DNA.

This reflects a deeper issue: banks are trying to graft new technologies onto old operating models. But platform-based, AI-driven banking requires fundamentally different ways of working. Without this shift, even the most advanced technologies will struggle to deliver meaningful impact.

The APAC opportunity and the risk of complacency

For APAC, the stakes are particularly high. The region is expected to lead CIB growth with a projected 7 per cent CAGR, outpacing both the Americas and Europe. This growth is driven by dynamic economies, expanding trade corridors and increasing digital maturity.

But growth can be deceptive. APAC banks may find themselves growing in absolute terms while losing strategic relevance if they fail to adapt to platform-driven competition. In a region where fintech ecosystems are particularly vibrant, the shift towards embedded finance and ecosystem orchestration may happen faster and more decisively than elsewhere.

Reinvention is no longer optional

The Capgemini report frames this moment as an inflection point. That may be an understatement. What we are witnessing is a structural transition from banking as a product-centric industry to banking as a platform-centric ecosystem.

The winners will not be those that digitise existing models, but those that reimagine their role entirely from financial intermediaries to orchestrators of value across networks.

For banks, the choice is stark. They can continue to optimise legacy models and gradually fade into the background of financial ecosystems. Or they can embrace the harder path by rebuilding their foundations and reclaiming their role at the centre of global finance.

The next decade of corporate and investment banking will not be defined by those that have the most capital but by those that control the platform.